3 Reg F Implementation Lessons from The GLCCA 2022 Conference

- May 19, 2022

- Category: Reg F

Recommended Reading

The Provana team recently joined the sixth edition of the GLCCA Conference where thought leaders from the ARM industry came together to discuss and exchange ideas that matter. The highlight of the conference was a two-part series on Reg F implementation. In the first session, the panel discussed “what’s next” in Reg F beyond the MVN, the E-Sign Act, and emails. In the second session, the focus was on the best Reg F practices, tripwires, and workarounds an agency should be aware of. Below are three key takeaways for collection agencies from these sessions.

1.There are plenty of gray areas in the law

Reg F is open for interpretation in places. For instance, CFPB doesn’t specifically give guidance about using aliases in any of the agency-consumer communication. Talking of consumer protection, harassment rules in Reg F are still not 100% clear, especially around textual communication. The GLCCA panel believed that embracing the ambiguity, but not letting your attention slip away is the best way forward.

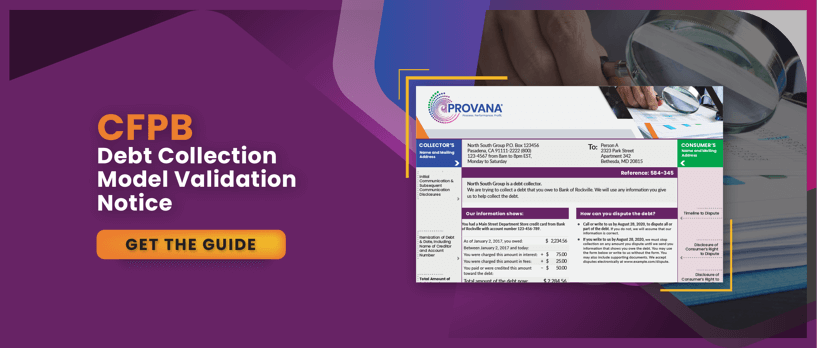

Remember consumer attorneys are largely looking for these gray areas where they can catch you faltering. For instance, it is not technically mandatory to use the exact demand letter template (also known as Model Validation Notice) provided in the rule. However, MVN is the place where most consumer attorneys are constantly looking for class-action lawsuit opportunities. Itemization date and itemization table seem to be the hottest MVN elements at the moment where agencies have been sued so far. So, learn to distinguish between the safe harbor and MVN. Make sure for “opt-out by the text” (one example of an exploitable weak spot for consumer attorneys), you capture variations of “stop” in all caps, lowercase, phrases, etc.

2. It is important to make every communication with consumers count

Experts believe that ‘Limited Content Message’ will eventually help agencies generate more inbound calls under the Reg F regime. To make the most of this touchpoint, include optional (but important) information in the voicemail such as the date and time of the message, dates and times for the consumer to reply, and the fact that they may speak to any of your agency’s representatives. The ease of access provided to consumers via this information can make a difference to any ongoing or future agency-consumer communication.

Given that CFPB has embraced omnichannel in a big way, it is also important to strategize for text communications under Reg F given most consumers (who don’t want to talk on the phone) are expected to opt for electronic communication in years to come. As you comply with the E-sign act, let consumers specifically know what requirements they will need to move forward with electronic communications.

3. Agencies need checks and balances to avoid delayed credit reporting

Under Reg F’s debt parking (the process of credit reporting the debt before communicating with the consumer) rule, agencies are required to send communication about the debt to the consumer. If that communication is in writing, they must wait a reasonable time (14 days) before they credit-report the account. The Bureau has also applied a 14-day “reasonable time” to electronic communications to ensure there are no deliverability issues, which could be a challenge. Hence, investing in a team/technology to monitor returned mail should be your top-most consideration under the latest CFPB rules.