Prepping for Reg F? Get These Tips to Improve Your Model Validation Notice Letters

- January 10, 2022

- Category: Reg F

Recommended Reading

The implementation date for the Consumer Financial Protection Bureau’s Regulation F (November 30, 2021) may have already passed, but many debt collectors are still preparing themselves to be fully ready to comply with the long-awaited rule. Under Reg F debt collectors, when contacting a consumer about a debt, are required to provide validation information to consumers, either orally or in writing. However, the written validation notice remains most common.

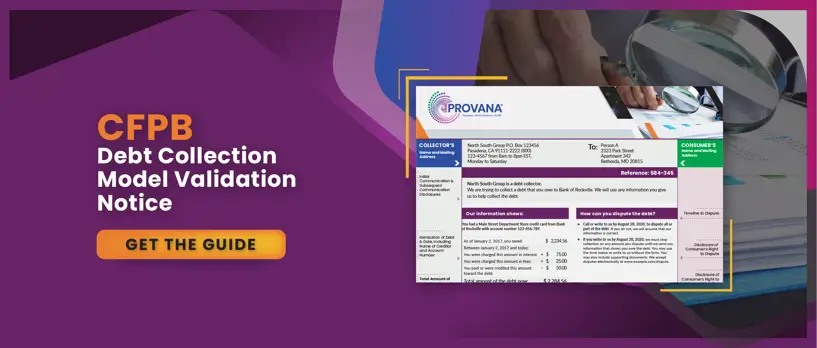

The rule contemplates that the validation information will be delivered via the validation notice. Reg F includes a debt validation notice template, also known as model validation notice (MVN), with new content and formatting guidelines. The rule provides certain legal protections to debt collectors who use the model validation notice to deliver validation information to consumers.

“Understanding the difference between required content and permissible content is important, because debt collectors who send letters which do not contain the required information will be at risk of violating the law,” says John Bedard, owner at Bedard Law Group.

This guide discusses different elements of MVN and how debt collectors can navigate the trickiest pieces of the demand letters. This guide should make it easier for debt collectors to incorporate the MVN template for demand letters into existing collection systems and make formatting and other permissible changes for Reg F.

Model Validation Notice Must-Haves

Collectors who use the model validation notice are protected by a “safe harbor” against claims that the collector’s letter does not comply the content and format requirements of Reg F. Those content requirements include:

- A debt collector communication disclosure (mini-miranda)

- Information about the debt, including

- Debt Collector’s name and mailing address

- Consumer’s name and mailing address

- Name of the original creditor as of the itemization date

- Account number

- Name of the creditor to whom the debt is currently owed

- Itemization date and amount of debt on the itemization date

- Itemization of the current amount of debt

- Current amount of debt

- Information about consumer protections

- Consumer-response information (attached in a tear-off format for paper notices)

Optional information to be included in Model Validation Notice

In addition to the information required to be contained in the Model Validation Notice, the rule allows a debt collector to include additional information in the MVN template for demand letter without losing safe harbor protections. The rule refers to these additional pieces of information as Optional Disclosures. Although the Bureau’s sample Model Validation Notice does not contain all the Optional Disclosures, here is list of those disclosures:

- The debt collector’s telephone contact information

- Information about electronic communications, including the debt collector’s website and email address.

- A reference code used by the debt collector to identify the consumer or the particular debt

- Certain specific language regarding payment options

- Disclosures required by, or that provide safe harbors under, applicable law

- Time-barred debt disclosures under certain specific circumstances

- Certain Spanish-language disclosures regarding how a consumer may request a Spanish language validation notice

- The merchant brand, affinity brand, or facility name associated with the debt.

Things to keep in mind

In line with other prohibitions mentioned in Reg F, there are certain to-dos that debt collectors must tick off from their list after extracting crucial information from the MVN.

- If a collector chooses to send the Model Validation Notice in additional languages, the rule instructs debt collectors to include both the English version and the translated version to the consumer in the same communication.

- The CFPB template does not specify any font requirements for MVN. Hence, in the case of written and electronic disclosures, the font size must be readily noticeable and legible to consumers. However, debt collectors should remain mindful of font size requirements imposed by state laws throughout the country.

- A disclosure should be mentioned in the debt validation notice, stating that the communication is in an attempt to collect a debt. Debt collectors utilizing the MVN will satisfy this requirement.

- If a validation notice is sent to a person who is authorized to act on behalf of the deceased consumer’s estate, the collector may write the name of the deceased consumer in place of “you” to avoid creating the impression that the authorized representative is personally liable for the debt.

- Debt collectors expecting to take advantage of the safe harbor should avoid adding additional language to the MVN template for demand letter or changing its format.

Things to watch out for

Though the model validation notice lists must-have information clearly, it still leaves some room for doubt, particularly around optional disclosures. This can, in turn, prompt debt collectors to make judgment calls regarding what to include and exclude in debt validation notices. For example, some may mix-up the account number and reference code number or think one is a substitute for another, leaving the consumer with insufficient or conflicting information.

The result? Debt collectors may put themselves at the risk of operating outside of a safe harbor or be subjected to an expensive lawsuit. Experienced regulatory attorneys or an expert auditor could add significant value by helping your agency navigate MVN template for demand letter and Regulation F. If you need help to steer the complexities of the new rule, click here.

Please note: This information is not intended to be legal advice and may not be used as legal advice. Every effort has been made to assure this information is up to date. It is not intended to be a full and exhaustive explanation of the law in any area, nor should it be used to replace the advice of your own legal counsel.

A contributor to this article was John H. Bedard, Jr., an AV-rated attorney and owner of Bedard Law Group. He is a recognized authority on the FDCPA and FCPA. Connect with John on LinkedIn here.