Credit Reporting in 2021 – 2 Common FCRA Violations and How to Avoid Them

- July 6, 2021

- Category: Complaints and Dispute Management

Companies in the credit and collection space have a slew of acronyms to contend with, and each comes with its own set of compliance requirements. To top it all, changes to Consumer Financial Protection Bureau (CFPB) rules and the Fair Credit Reporting Act (FCRA) / e-OSCAR dispute resolution is only making it more challenging for credit and collections organizations.

Not paying attention to the details of compliance can prove costly. While establishing an automated compliance management program can help, it’s important to keep informed on the latest rule changes, especially since there seem to be weekly status updates.

Compliance is no joke. In 2019 alone, the Federal Trade Commission permanently barred 23 individuals and companies from working in the debt collection arena and collected $24.7 million in judgements from court cases in unlawful debt collection practices.

Since the introduction of the FCRA in 1970, the organization has put the responsibility of fair reporting on data furnishers to ensure that they are meeting all federal requirements and state statutes. Broadly, FCRA violations can be put into two buckets:

- Erroneous Information Reporting

- Violation of Debt Dispute Procedures

1. Erroneous Information Reporting

Reporting information that is not verified and thus, is outdated or incorrect is one of the most common reasons for consumers disputing their information.

On paper, this issue could look like:

- Wrongly noting the total amount due or “overbidding”

- Mis-stating the amount collected

- Inaccurately reporting the time of payment

- Not removing outdated information (7 years in case of credit and 10 in case of bankruptcies)

- Misrepresenting the actual debtor (connecting the debt to a relative or a different individual with the same name who lives in the same house because of Jr./Sr. issues)

- Incorrectly reporting the credit rating

Since the information is not verified and accurately represented, it is grounds for being reported for violation of the FCRA.

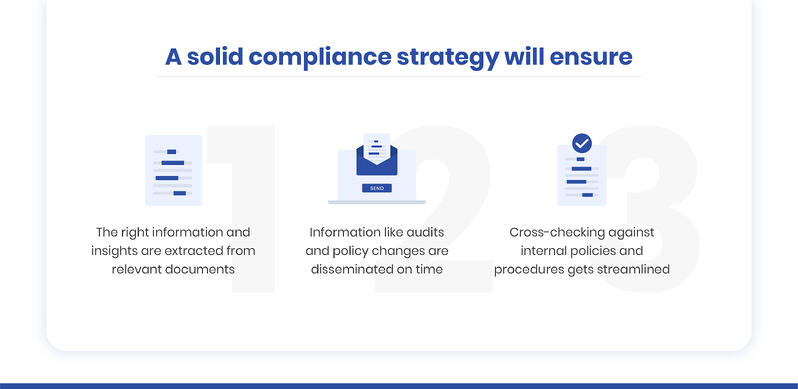

A solid compliance strategy will ensure that:

- In-house quality checks are performed to extract the right information from the relevant documents

- Information is disseminated in time

- Cross-checking against internal policies and procedures

2. Violation of Debt Dispute Procedures

Debt dispute is another challenge that plagues the collection industry. If a consumer has reported an issue with a collection, it is the duty of the firm to investigate and report it correctly.

The CARES act mandates data furnishers to continue reporting to Credit Reporting Agencies (CRAs), which impacts consumer credit reports. Some of the most common ways a firm can violate debt dispute procedures include:

- Failing to include reported information about the dispute

- Failing to include the results of an investigation up to “reasonable” standards

The volume of disputes can make it hard to keep track of additional material. A more streamlined approach would be to establish an automated workflow where once you receive additional information about a dispute, you can:

- Confirm that the material has been received

- Track that the confirmation is communicated to all parties involved

- Disseminate the information to relevant stakeholders for processing

- Ensure compliance with dispute resolution timeframes

Although courts could potentially allow data furnishers and CRAs more time to investigate disputes in view of COVID, the decisions will be made on a case-by-case basis and the courts still expect agencies to act in “good faith”. Such violations can still lead to infractions – and an automated dispute management solution can help you avoid these challenges while simultaneously cutting your expenses.

Moreover, you should have a bird’s eye view of all processes to ensure they are complying with all the regulations. This is where an automated compliance management program can help you ensure efficiency and prevent liability where collections are concerned. It can also give you a transparent view into how disputes are being resolved by agents in the company and triggers notifications if company’s standards are not met.

If you need any help streamlining your dispute management, reach out to us now!